Essay

No. 041

26 March 2026

12 min read

GTM Strategy

Why marketing is measured like a revenue function and controlled like a cost center

Read the 1st episode here, 2nd episode, 3rd episode

Not everything that can be counted counts, and not everything that counts can be counted.

A marketing leader I know left a company last year with an impressive résumé line: 30% pipeline growth, year-over-year. The number was real. Verified, attributed, reported at the board level. The dashboards were clean, the trajectory upward, the narrative easy to defend in any boardroom. The system had responded exactly as designed.

Six months after his departure, the cracks began to surface. Win rates softened. Sales cycles stretched. Discounting increased. Brand-driven inbound had quietly halved as a share of total pipeline. The volume was still there, but its quality had changed. More was required to achieve the same outcome. Then more again. Nothing in the dashboards had anticipated this shift, nor suggested that the underlying system had been weakening while visible indicators improved.

This is not a story about a bad marketer. It is a story about what happens when a function is evaluated on what can be measured rather than on what actually drives outcomes.

The previous articles in this series examined how SaaS marketing shifted its objective from building durable demand to maximizing pipeline contribution, how measurement infrastructure encoded that shift, and how attribution manufactured the quarterly evidence that made the shift feel rational. This article asks a different question: what did it cost in the long term ?

What follows is not a critique of marketing execution. It is an examination of the financial logic that governs it.

From a financial perspective, the logic is internally consistent.

A CFO does not allocate capital based on intuition. Capital is allocated based on visibility, comparability, and defensibility. What appears in a spreadsheet, what can be tracked over time, what can be linked, however imperfectly, to financial outputs, is what can be funded. Marketing adapted to this constraint. It became legible, translating activity into numbers that resemble financial outputs, and in doing so gained legitimacy, budget, and a seat at the revenue table.

But in accepting this framing, marketing accepted a deeper transformation: it now operates as a two-tier system governed by two distinct loss functions.

Loss Function A: demand creation — long-loop, diffuse, non-attributable, shaping the conditions under which pipeline exists

Loss Function B: demand capture — short-loop, measurable, attributable, directly connected to pipeline.

Only one produces quarterly evidence and is consistently funded. The other determines whether that evidence has any economic meaning, yet struggles to justify investment within the same system.

The system does not optimize for performance, it optimizes for what can be defended. Activities that produce immediate, attributable outputs sustain themselves in allocation decisions. Activities that shape perception, preference, and category understanding operate upstream, with delayed and distributed effects, and are therefore structurally deprioritized.

The result is a structural misalignment that no org chart redesign has resolved. This is not a management problem. Modern marketing operates as a financial misclassification, followed by a misallocation of capital under partial visibility.

Marketing is funded like a cost center and evaluated like a revenue function. It is expected to produce pipeline with the discipline of a revenue engine while operating with limited control over the variables that shape that outcome. The question it is regularly asked is not “What system did this investment improve?”, but “What did this campaign generate?”

Image created with GPT Image 1.5 High Fidelity

Compare marketing to the functions that sit alongside it.

Sales operates in short loops. It controls activity, coverage, execution, and, to a significant extent, conversion. Revenue is realized at the end of its process. The link between input and output is direct enough to support investment logic. Budget in sales is treated as an investment in capacity: more reps, more coverage, more potential revenue.

Product operates on longer loops, but with a different form of control. It owns the core variables that define value: product quality, feature set, user experience, and increasingly, pricing. The relationship between product decisions and user behavior can be observed, tested, and iterated on within a relatively closed system. Product investment is justified through coherent causal narratives, even in the absence of direct revenue attribution.

Marketing occupies a hybrid position without the benefits of either model. It has short-loop levers—campaigns, targeting, channel optimization—but these do not produce outcomes with the immediacy or controllability of sales. It influences long-loop variables—preference, positioning, category framing —but does not own them in the way product does. It operates in an open system where pipeline performance is shaped by product quality, pricing strategy, market positioning, brand preference, as well as market conditions and competitive dynamics. Marketing contributes to each, but controls none end-to-end. And yet it is evaluated as if it did.

No function owns demand in its entirety. But marketing is held accountable as if it were the integrator of all upstream and downstream effects: funded like a short-term expense, expected to build long-term demand, and held responsible for outcomes that depend on upstream variables it does not fully control. This is not a case of asking a fish to climb a tree. It is a case of measuring the tree, ignoring the water, and then holding the fish accountable for both.

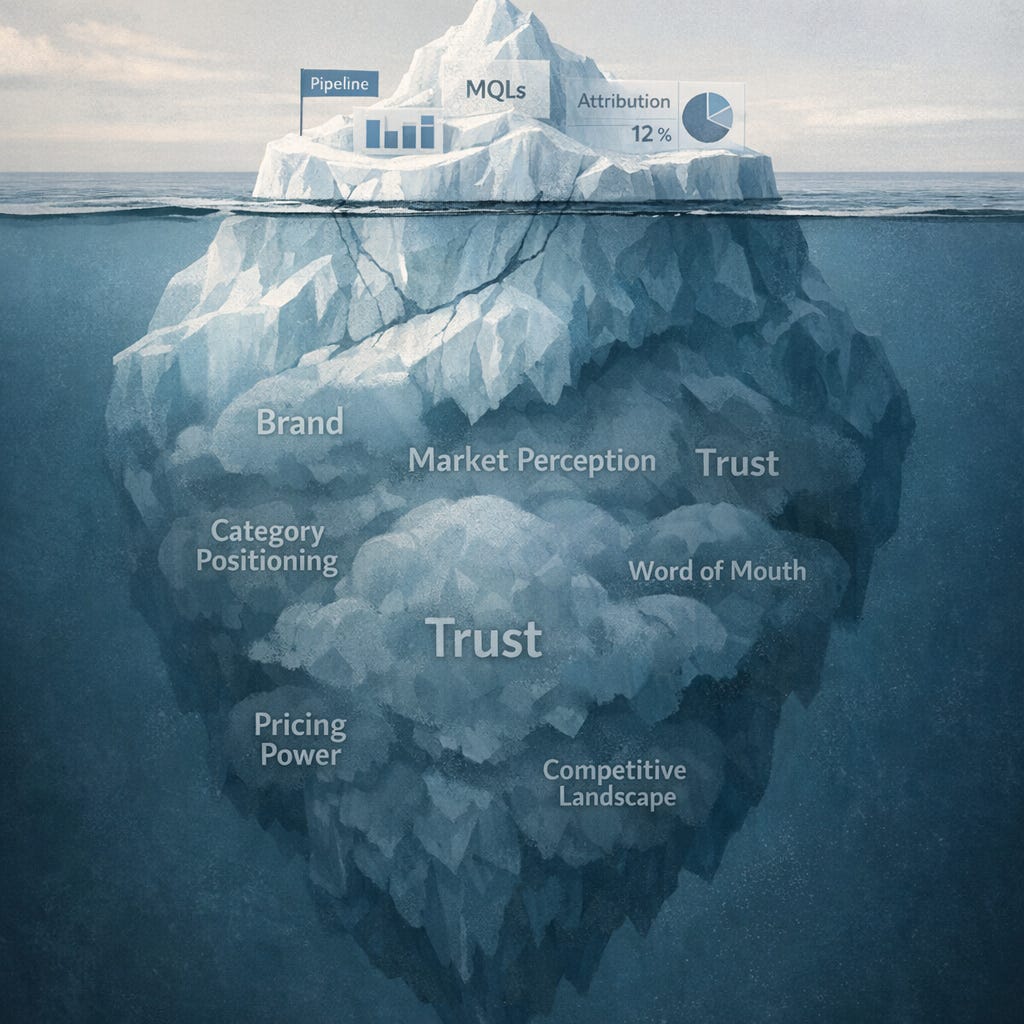

Within this system, one component is consistently deprioritized: brand.

This is not because brand lacks impact, but because it operates precisely where the system is least capable of measuring : upstream, over time, across functions. It is also the component that determines whether the entire pipeline machine produces durable value or merely temporary volume.

In SaaS, the word “brand” is used constantly and almost never defined with precision. Part of the confusion comes from reducing brand to its artifacts—the logo, the color palette, the guidelines document, the tagline. These are outputs of a brand that may or may not exist. Brand itself is something else entirely: it is the answer the market holds about you when you are not in the room.

Its economic role is more fundamental. Brand shapes preference, frames how buyers define their problem, increases the likelihood of being considered, and aligns the solution with the buyer’s context.

Marketing is funded like a short-term expense, expected to build long-term demand, and held responsible for outcomes that depend on upstream variables it does not fully control.

It acts before pipeline exists, and conditions both its formation and its conversion. Two economic functions emerge from this role.

As an ice-breaker, brand determines whether you enter the conversation at all: whether your name appears on the shortlist, whether an email is opened, whether a meeting is accepted. The first solution a buyer thinks of when a need arises is rarely the result of a recent campaign: it is the outcome of accumulated exposure, often built long before any trackable event.

As an insurance mechanism, brand reduces the perceived risk of the decision. In uncertain environments, buyers gravitate toward what feels known, credible, and established. The old adage “Nobody ever got fired for buying IBM”captures this dynamic. While dated in expression, it remains accurate in its logic: brand lowers the personal and organizational risk associated with choice. Two companies may offer comparable products within the same category, the one backed by stronger market recognition operates under entirely different conversion conditions.

These two functions reinforce each other over time. Entering more conversations builds familiarity, familiarity increases trust, trust improves conversion, conversion reinforces visibility. The effect compounds over time. A company without this dynamic must recreate it artificially through pipeline activity, one interaction at a time, at significantly higher cost and with no cumulative advantage.

In SaaS, building a brand means something specific. It is not primarily an exercise in visibility or advertising, but in shaping the structure of the market itself. The most effective form this takes is category creation and control: naming the problem, educating the market, influencing how buyers articulate their needs, and positioning certain solutions as the natural answer. This is brand as infrastructure of demand creation, not an overlay on demand capture. Let’s consider two examples.

Brand is the answer the market holds about you when you are not in the room.

Gong did not enter a market defined as “call recording” and compete on incremental features. It articulated “revenue intelligence” as a category, built a sustained content engine around a point of view on how revenue teams should operate, and diffused that vocabulary into the market. By the time many buyers entered a formal buying process, the terms of evaluation had already been shaped. The category existed before the pipeline, and it existed on Gong’s terms. In that context, pipeline performance became easier to explain, not because attribution improved, but because the upstream conditions that determine pipeline quality had already been structured.

Drift provides the case that shows where the structural limit sits. It invested early in defining “conversational marketing” as a category, built a point of view the market adopted, and for several years produced the kind of differentiation and pricing power that competitors running standard demand capture playbooks could not replicate. The demand creation worked. Then the competitive landscape caught up — over 160 vendors emerged across adjacent segments — and the category itself began to commoditize around the very vocabulary Drift had created. In 2024, Vista Equity Partners, which held majority stakes in both Drift and Salesloft, merged the two companies. The brand had done what brand is supposed to do. The fund cycle and the competitive dynamics operated on a different clock. A system built for long-term demand creation was absorbed into one optimized for capital efficiency and portfolio consolidation.

Taken together, these examples illustrate both the power and the boundary of brand in SaaS. It can define markets, structure demand, and materially alter the efficiency of the revenue engine. But it operates within broader economic systems, competitive and financial, that may not reward those effects on the same timeline.

In SaaS, these activities take specific forms: thought leadership that shapes how the industry thinks rather than content that follows existing demand; original research that becomes reference material rather than derivative output optimized for distribution; community structures where customers reinforce their own conviction; executive visibility, customer advocacy, and ecosystem presence that embed the company into how the market operates, not just how it evaluates solutions.

What these activities share is not their format, but their economic profile. Their impact is distributed, delayed, and non-isolable in financial terms. They do not produce attributable pipeline within the quarter in which they are executed. Their effects appear indirectly, through changes in downstream variables: win rates, sales cycle length, pricing power, demand resilience, expansion, and customer acquisition cost.

And this is where the system reasserts itself.

Under pipeline accountability, these contributions struggle to compete for budget, not because they lack impact, but because their impact operates through long-loop, distributed causality in a system built to reward short-loop, isolable returns. This is the mechanism that makes brand the most consistently underfunded strategic asset in SaaS.

Ownership structure further reinforces this dynamic. Brand compounds over years. Venture capital fund cycles operate on five to seven years, with exit pressure building from year three. Private equity operates on three to five. Investing meaningfully in an asset whose returns will not be visible within the fund cycle, within that incentive framework is a misallocation.

In venture-backed companies, the pressure is velocity. Growth targets are reverse-engineered from valuation expectations. Marketing is pushed toward immediate output, even as that output becomes progressively more expensive. The initial hypergrowth looks compelling on the fundraising deck. The decline that follows appears inexplicable—but it is the same mechanism in reverse: growth was funded by capital, not sustained by market preference, and when capital slows, there is no accumulated demand to carry the momentum.

In private equity environments, the pressure is margin. Marketing is treated as a cost base to optimize. Investment shifts toward activities that demonstrate short-term return, even as the underlying demand environment weakens.

In public companies, the pressure is narrative. Quarterly expectations require consistent, defensible performance. Pipeline provides that narrative. The system rewards predictability over structural strength, even when the two begin to diverge.

In founder-led companies, the dynamic plays out differently, but not fundamentally. The spiral is often slower because strategic control remains more integrated: positioning, product direction, and go-to-market are still connected through a single line of judgment. In some cases, this allows brand investment to be sustained long enough to function as infrastructure rather than discretionary spend. But this remains contingent on the founder’s ability to maintain that coherence under external pressure.

Across these contexts, the pattern holds: brand is acknowledged in principle, but underfunded in practice. The system that allocates capital does not explicitly reject it, but simply fails to register its effects in time or in isolation.

Demand capture is a treadmill. You run hard, you stay in place, and the moment you stop, the motion stops with you. Demand creation is an escalator. You invest, it compounds, and even when you step off, the momentum continues to carry you forward. The financial logic of the last decade pushed SaaS marketing almost entirely onto the treadmill.

The consequences accumulate below the threshold of quarterly reporting. Pipeline quality degrades, requiring ever greater volume to sustain revenue targets. Customers acquired without conviction churn faster. Pricing weakens as every deal becomes a negotiation. Sales effort expands to compensate—more outreach, more follow-ups, more discounting—while the marginal return on each additional dollar declines. The system does not collapse, it intensifies. More input is required to produce the same output.

What makes this dynamic particularly difficult to detect is that the dashboard remains coherent while the economics deteriorate. Pipeline volume can hold, even grow, because declining efficiency is offset by increased spend. The metric that governs the function cannot detect the failure mode the function is experiencing.

Modern marketing operates as a financial misclassification, followed by a misallocation of capital under partial visibility.

At the same time, the interpretation of that metric shifts with market conditions. The measurement system is not the causal system, yet the two are routinely conflated. In periods of growth, demand is abundant and buyers arrive with pre-formed intent. Outcomes are favorable, attribution appears consistent, and the system seems valid. In periods of constraint or saturation, the same framework begins to fragment. Conversion paths elongate, attribution weakens, and the link between activity and outcome becomes unstable. What changes is not causality itself, but the system’s ability to represent it.

This asymmetry creates a structural misreading. In growth, correlation is accepted as evidence of causation. In decline, the breakdown of measurement is interpreted as a breakdown of execution. Marketing is held accountable for outcomes shaped by upstream conditions that were never measured, and therefore never managed.

By the time the deterioration becomes visible, the damage is structural and the recovery timeline extends beyond quarters into years. Spend can be increased quickly, preference cannot. In many cases, the more difficult realization follows: the demand that needs to be rebuilt was never truly created. The system made its absence invisible by substituting activity for accumulation.

The bill arrives late. And when it arrives, its impact is larger than anticipated, because the compounding was never accounted for, and neither was the gap between what was measured and what was actually driving the outcome.

The résumé says 30% pipeline growth. The market says something different. Both are telling the truth. They are answering different questions.

The question that actually determines whether the company wins — whether marketing is creating the conditions for efficient, sustainable revenue growth — does not appear on any dashboard. It exists upstream of pipeline, attribution, and quarterly metrics.

This article has examined what that structural defect costs a single company. The next asks what happens when the same defect operates across an entire industry, when a thousand companies build the same pipeline machine, compete on the same playbook, and discover, at the same time, that the market has been quietly withdrawing consent.

That convergence, and what survives it, is the subject of the final article.

Read the Episode 1, Episode 2, Episode 3, Episode 5. Subscribe to follow the argument as it develops.

Keep reading